Bitcoin (BTC) hit ten-day lows at Tuesday’s Wall Street open as BTC price action followed a US stocks sell-off.

Key points:

- Bitcoin price action reacts to contagion from an Asia stocks sell-off as it hits US markets.

- Chip makers are at the epicenter of the reversal with South Korea’s KOSPI Index closing the day down 10.8%

- Crypto long liquidations pass $500 million in 24 hours.

Semiconductor giants fuel major Asia stock comedown

Semiconductor-led losses from Asia spilled over into US trading. South Korea’s KOSPI Index finished the day down 10.8% in a single session, fueled by 14.8% losses for chip-maker SK Hynix, while Japan’s memory manufacturer Kioxia Holdings fell 18.3% on the day.

In the US, the tech-heavy Nasdaq Composite Index was down just over 1% at the time of writing. Notably, semiconductor manufacturer Micron Technologies, which fell by more than 10% at the open, erased a rebound and saw its lowest levels since May 22.

Micron Technologies one-week chart. Source: Cointelegraph/TradingView

Semiconductor stocks are contending with intensifying scrutiny over the sustainability of hyperscaler capital expenditure. Investors increasingly question whether the underlying economics of AI infrastructure buildouts can justify their scale. Combined 2026 capex guidance from Alphabet, Microsoft, Amazon, and Meta is now tracking toward $725–730 billion, with Wall Street projecting that figure could climb toward $900 billion in 2027. Alphabet posted its first cash burn on record in the second quarter, at $5.9 billion, even as its cloud unit posted 82% growth.

Layered on top of the financing concerns are competitive pressures on US-based AI companies from Chinese startups. Moonshot AI’s Kimi K3 open source model, first launched two weeks ago, was benchmarked competitively against top proprietary systems from Anthropic and OpenAI. This has intensified questions about the return profile assumed by the spending commitments of Western hyperscalers, given their capabilities may be replicated at a fraction of the cost.

Crypto short liquidations pass $500 million

Today’s sell-off in the semiconductor and AI sector has not left Bitcoin unscathed. Data from TradingView showed BTC/USD dipping below $63,000 for the first time since July 17.

BTC/USD four-hour chart. Source: Cointelegraph/TradingView

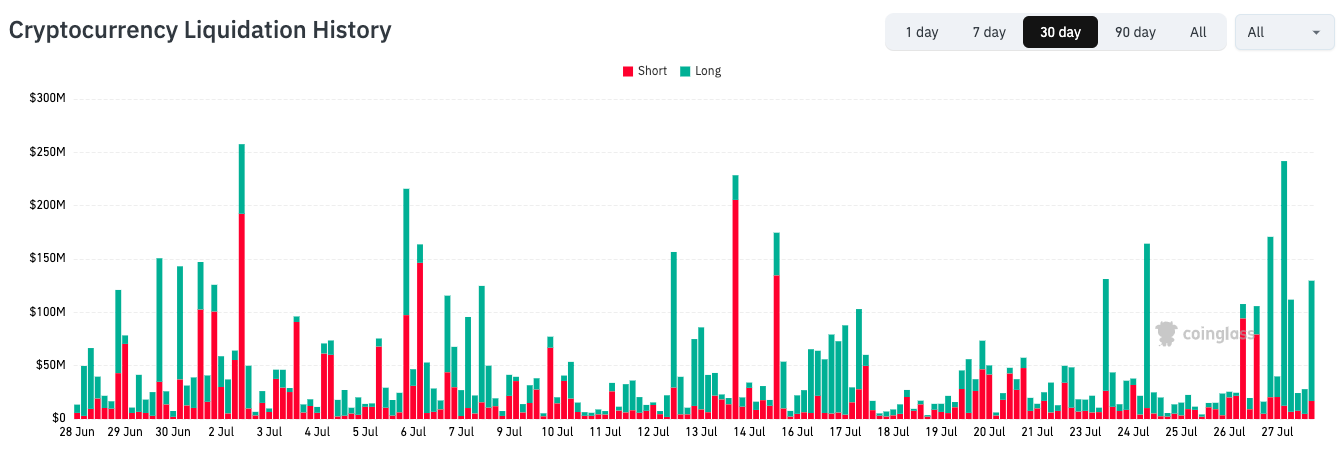

Crypto markets saw elevated long liquidations on the back of the day’s reversal, with data from CoinGlass putting these in excess of $510 million over 24 hours.

Related: Markets eye Bank of Japan meeting on Friday as yen repeats 40-year US dollar lows

Cryptocurrency liquidation history (screenshot). Source: CoinGlass

On Monday, crypto analytics platform CoinAnk warned of the risk of a long liquidation “cascade” below $64,700.

“Extremely large long liquidity has accumulated below this level,” it commented.

CoinAnk added that to the upside, little resistance remained, with the area between $65,800 and $66,200 being a “major short liquidation zone.”

Announces its Participation in World Foundation’s $52.5M funding round")

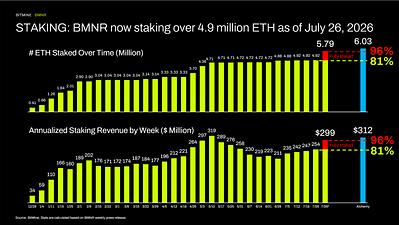

Announces ETH Holdings Reach 5.79 Million")